Analysis of crude oil price movement for August 2025, combined with insights into market drivers and a projection for September. All data is sourced for clarity and reference.

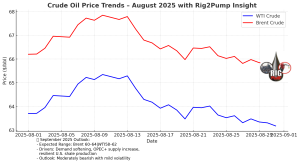

August 1–31, 2025: Crude Oil Price Trends

Observed Price Movement – WTI Crude (Cushing)

According to daily WTI closing prices from the Federal Reserve’s FRED dataset:

- August 19: ~$63.38

- August 20–22: Modest climb to ~64.19–64.56

- August 25: ~65.18

- August 29: Brief dip to ~64.01

- August 31: Ending around ~63.96

Key Contextual Highlights

- Early August Surge: Following production cut doubts and supply tightness, WTI rallied to ~$66–67 before the month began—an extension from July’s momentum

- OPEC+ Supply Increase Announcement: In early August, OPEC+ unveiled a 548,000 barrels/day production boost, tempering supply fears and contributing to downward price pressure

- Softening U.S. Demand & Rising Inventory Concerns: As summer demand waned, traders grew cautious, weighing this against impending autumn supply increases

- Moderate Market Stability: Despite geopolitical tensions cooling and markets remaining relatively calm (Brent hovering around $67–70), overall volatility slipped to near historic lows

August Summary: Crude Price Momentum

| Period | Price Trend | Market Sentiment & Drivers |

| Early August | Reached ~$66–67 | Supply concerns, OPEC+ cuts, tight output projecting higher |

| Mid-August | Stabilized ~63-65 | OPEC expansion, reduced demand, inventory builds |

| Late August | Slight decline (~64) | Weak demand signals and supply normalization |

September 2025 Projection

Based on current trends and analyst forecasts:

| Forecast | Brent | WTI |

| Expected Range | $60–64 | $58–62 |

Why This Projection Holds:

- Seasonal Demand Softening: With summer ended, lower driving and industrial activity typically cools demand

- Supply Ramp-up by OPEC+: Continuation of production boosts may create a mild surplus, exerting downward pressure

- Cautious Forecasts from Analysts: Institutions like Goldman Sachs peg Brent at ~$64 in Q4 with downside risks, and many expect continued market softness into 2026

- US Production Resilience: Despite low prices, shale growth could persist—limiting upward price swings

Rig2Pump Insights

- August 2025 saw crude prices driven by a mix of supply-tightness fears, strategic OPEC+ outputs, and cooling demand trends—resulting in a mild decline from early highs (~$66) to ~$64 WTI.

- Looking ahead to September, prices are likely to remain moderate to slightly lower, influenced by OPEC+ actions, seasonal demand shifts, and sustained shale supply.

No comment